Not many ordinary people who do not major in economic are perfectly aware of the difference between fiscal policy, and financial policy. This term comes out when the media reports economic news, but it is true that it is vague. This time, I would like to talk about these three economic policies. Before and after you read this article, please experience the difference between you and understand economic news.

S.Korea's fiscal policy, monetary policy, financial policy in 2023

Shortcuts to economic analysis(exports, consummer prices, private debt, etc.) in 2023

Fiscal policy encompasses all government policies that use government spending and taxes as a policy tool. The objectives of fiscal policy generally include full employment, price stability, balance of payments, economic growth, and income redistribution.

Monetary policy refer to a policy that allows the central bank (rhe Bank of Korea), which has exclusive issuance power, to achieve price stability and financial stability by affecting the amount of money or interest rates, so that the economy can achieve sustainable growth.

The central bank did not carry out monetary policy from the beginning, but the Great Depression in the 1930s allowed many countries to abandon the gold standard, allowing the central bank to issue money with disconnected gold pipes and supply money at its discretion.

Monetary policy refers to monetary policy or monetary credit policy, in which monetary authorities regulate the amount of money or interest rates to stabilize and grow the economy. The government uses direct and indirect controls to achieve the best monetary policy goals of price stability and financial stability. These measures include central bank lending policies, reserve requirements and open-market manipulation policies, as well as controlling new interest rates and financial availability.

Shortcut to Korea's Economic Crisis in 2023

Fiscal policy

The 2023 budget is considered th have emphasized fiscal soundness compared to 2022. The fiscal dificit and national debt relative to GDP narrowed from the 2022 budget as the growth rate of total expenditure (5.2%) fell below the growth rate of total revenue (13.1%).

◎ Management fiscal deficit (% of GDP): ('18) 0.6 → ('19) 2.8 → ('20) 5.8 → ('21) 4.4 → ('22) 4.4 → ('23) 2.6

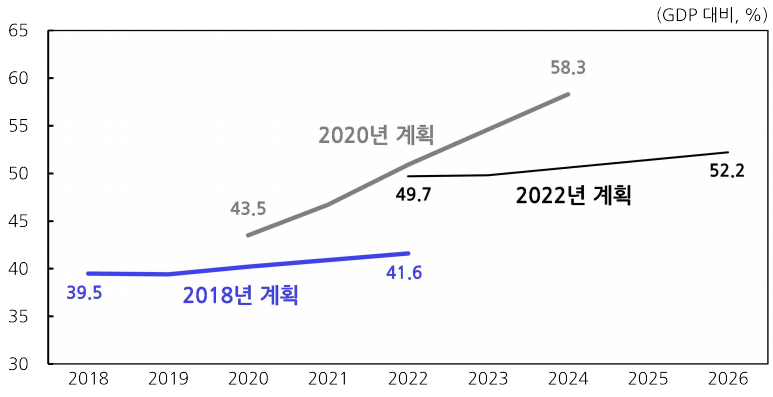

◎ National Debt Ratio (% of GDP): ('18) 35.9 → ('19) 37.6 → ('20) 43.6 → ('21) 46.9 → ('22) 50.0 → ('23) 49.8

<Key Financial Indicators>

Reference) The economic growth forecast applied the premise of the 2022-2026 National Financial Management Plan.

By detailed item, it is evaluated that it focused on economic structure transformation and support for the vulnerable rather than economic stimulus in cooperation with the monetary authorities' policy stance that values price stability. There is a possibility that the economy will slow down in 2023, but rather than short-term economic stimulus, the budget has been focused on spending to secure mid-to long-term growth potential.

Shortcut to 2023 Budget(Definite Budget)

It seems desirable to adjust the soaring spending of the COVID-19 crisis and emphasize fiscal soundness in the mid-term fiscal plan, and it is necessary for the government to come up with efficient fiscal management measures to improve sustainability. It is planned to maintain the mational debt ratio at around 50% in the medium term by managing fiscal expenditures that expanded the COVID-19 response in the 2022-2026 National Financial Management Plan.

The ratio of national debt to GDP was planned to be around 40% before COVID-19, but it was revised to gradually increase to late 50% range during the COVID-19 crisis, and it was lowered again in 2022.

<Changes in the national debt ratio in the national fiscal management plan before and after COVID-19>

It is urgent to secure fiscal capacity and improve fiscal sustainablility by flexibly adjusting the financial structure according to changes in the demographic structure such as low birth rate and aging population. As fiscal demand is expected to surge due to changes in the demographic structure, there is a high need for preemptive fiscal capacity and fiscal soundness management, and the introduction of effective fiscal rules can be one of many measure. It is necessary to come up with a rational adjustment plan for sectors where fiscal demand is rather reduced due to changes in the demographic structure, such as local education and financial grants.

Monetary policy

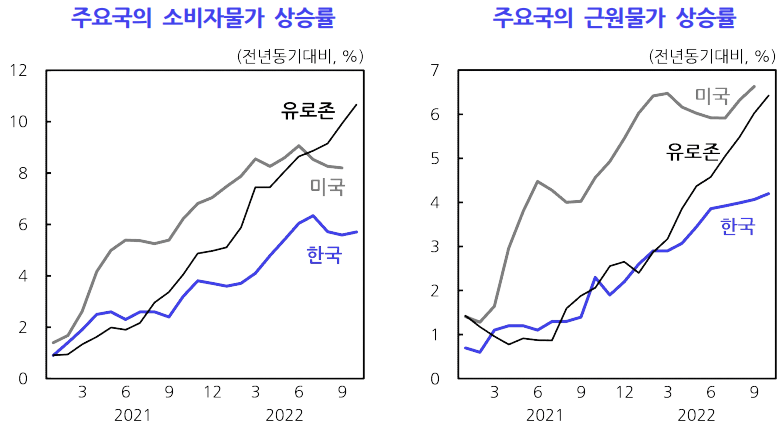

It is necessary to maintain the base rate hike stance for the time being so that expected inflation does not become unstable, but to determine the pace of the rate hike by considering the possibility of an economic slowdown. Since the fourth quarter of 2021, inflation has significantly exceeded the inflation target (2%), requiring monetary policy response.

However, from the perspective of operating monetary policy in a future-oriented manner, it seems necessary to raise the benchmark interest rate at a gentle pace in consideration of the possibility that the economy will shrink excessively in the future. In consideration of the ripple parallax of monetary policy, the policy stance should be determined, focusing on prices and economic trends expected in the future.

As raw material prices gradually stablize in the future and the Korea economy enters an economic slowdown, both supply-side and demand-side inflation pressures are expected to decrease. It is necessary to consider that a rapid rise in market interest rates at a time when private debt is high could dampen the domestic economy.

Note) Core prices refer to consumer prices excluding food and energy, the fourth quarter of 2022 is October figure, and household loan interest rates are based on new handling amount.

Meanwhile, Korea's monetary policy needs to be operated around domestic prices and economic conditions. Recently, policy interest rates have been raised steeply in the United States and the Eurozone, but given the conditions of our economy, such a rapid rate hike is not required. As you can see from the table below, the inflation rate in the United States and Eurozone is significantly higher than that of Korea.

In line with the purpose of the autonomous floating exchange rate system, it is necessary to tolerate exchange rate fluctuations and carry out monetary policy focusing on domestic macroeconomic stability such as prices, the economy, and the financial system.

In addition, monetary authorities must deal with the tightening of foreign currency liquidity and the resulting financial system risk if the foreign currency fund market becomes unstable.

Considering the basic economic conditions of Korea, it seems unlikely that a sharp capital outflow and a foreign currency liquidity crunch will occur. Nevertheless, if the foreign currency funds market becomes unstable, it should focus on preventing temporary foreign currency liquidity crunch in financial institutions from spreading to financial system risks rather than directly responding to superficial symptoms such as exchange rate hikes.

Financial policy

While maintaining the stance of strengthening macroprudentiality, it is necessary to pay attention so that system risk management does not lead to poor accumulation, and to re-examine the preliminary management system. Banks' corporate loans are constantly increasing, But the financial market is showing instability, with a temporary crunch due to a rapid decrease in the supply of funds in the bond market.

Amid concerns over worsening non-bank financial statement (B/S) as asset price adjustments due to rising interest rates increase the possibility of insolvency of real estate PF loans and asset-backed securities, the issuance of blue-chip corporate bonds and financial bonds remains high, causing a temporary credit crunch in the corporate bond market.

The higher the risk of financial market instability, the more efforts are required to strengthen financial soundness while cleaning up insolvent assets. Household debt growth has been controlled since the fourth quarter of 2022, but corporate debt has continued to expand. It is necessary to strengthen the resilience of our economy to internal and external shocks by gradually normalizing the soundness regulations eased in the COVID-19 crisis.

Therefore, policy intervention to mitigate the credit crunch is necessary only if some assets are likely to be transferred to system risk. In order to ease the credit crunch, it is necessary to supply funds concentrated in the banking sector to the market where the credit crunch occurs through bond market stabilization funds.

ㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇㅇ

On the other hand, each financial institution should understand the importance of system risk and prepare a similar level of soundness management mersures for the financial institution. In particular, since late 2018, as non-bank financial institutions have become similar in asset size to that of bank assets, the need to manage system risks caused by insolvency of non-bank financial institutions has increased.

Note) Vulnerable borrowers refer to borrowers who are 'income below the 2nd quintile' or 'below the bottom 20% (700 point) of credit rating'.

It is urgent to flexibly operate the legal maximum interest rate in preparation for the risk of refinancing vulnerable households and small business owners due to soaring interest rates, and to protect vulnerable borrowers in preparation for an economic slowdown.

"Those who sleep over their rights can never be protected."

a useful article to read together

2023년 한국경제 위기론

한국의 2023년 1월 무역적자가 2008년 글로벌 금융위기 때 1년 동안 발생한 무역적자에 육박하는 수치를 기록했습니다. 즉 가장 나빴던 해의 1년 치 무역적자를 한 달 만에 거의 도달한 것입니다.

bhtm100.com